ai

Big Tech, Big Bonds

On Tuesday, SpaceX filed its IPO prospectus. The headline number is staggering — a $1.75 trillion valuation, with $50–80bn of equity to be raised. It would be the largest IPO in history by a wide margin. But the more interesting story isn't about the IPO market, it's about the bond market.

The biggest capital markets event of the year just fired its starting gun: on Tuesday, SpaceX filed its IPO prospectus. The headline number is staggering — a $1.75 trillion valuation, with somewhere between $50bn and $80bn of equity to be raised. It would comfortably be the largest IPO in history, dwarfing Saudi Aramco's previous record of $25.6bn.

But, while the equity market is getting all the headlines, it's the debt market that has been quietly transformed by the tech sector over the past few years - in ways that many people haven't noticed.

The bond market belongs to Big Tech now

Consider a fact that ought to be more widely discussed: AI-related debt is now roughly 15% of the US investment-grade corporate bond market, having quietly overtaken US banks as the largest single sector.

The numbers behind that shift are dramatic. According to BofA, the big Five hyperscalers (Amazon, Alphabet, Meta, Microsoft, Oracle) issued $121bn of bonds in 2025, against an annual average of $28bn between 2020 and 2024. BofA expects them to issue $140bn per year for the next three years, possibly $300bn at the upper end. At those levels, hyperscalers as a group would match the Big Six US banks ($157bn/year) for issuance volumes. Dell'Oro projects $1.7 trillion of global data centre capex through 2030, with the top four US hyperscalers representing roughly half. This needs to be funded.

The landmark deals are starting to define the IG calendar. Meta's $30bn October 2025 print was the largest non-M&A high-grade bond sale to date. Oracle, Alphabet and Amazon all followed with $15-$18bn deals in the same quarter. Between them, hyperscalers accounted for four of the five largest US high-grade bond deals of 2025.

From tax arbitrage to industrial capex

This wasn't always so. Big Tech's first major foray into the bond market, a decade ago, looked nothing like this.

Apple's debut bond in April 2013 - $17bn, then the largest corporate bond sale ever attempted - made little sense at first glance. The company had $145bn of cash on its balance sheet. Why borrow? The answer was that the cash was offshore, and repatriating it would have meant a 35% tax bill. Section 956(c)(2) of the US tax code allowed companies to sidestep this if their overseas cash was invested in US Treasuries and domestic corporate securities. Apple, Microsoft, Google and Cisco collectively held $163bn of US government debt offshore by 2014. Quietly, they became one of the largest fixed-income investor blocs in the world. Issuing domestic bonds at sub-3% to fund buybacks and dividends was a tax trade, not a capital-raising one. The 2017 TCJA cut repatriation tax to 15.5% and shifted to a territorial system. The trade died, and big Tech largely stayed out of the bond market for the next five years.

What's happening now is structurally different. This is real industrial capex: GPUs, fibre, substations, land, water-cooled buildings the size of small towns. The right comparison is no longer to the consumer-tech treasury operations of the 2010s. It is to the capital-intensive industries that built earlier waves of the American economy: railroads, autos, oil and gas, mining. The bond market has always been the financing mechanism for industrial-scale infrastructure. What's novel is that the infrastructure now lives inside server racks.

The Colossus data centre. Source: xAI

The inference bottleneck

For the first 18 months of the GenAI era, the compute story was about training. Bigger models, larger runs, longer epochs. This was bursty and capex-intensive, but ultimately one-off per generation. What's shifted over the last six to twelve months is that inference (ie running the models, every day, for every user) has become the dominant compute load. Inference is fundamentally different from training: it's continuous, latency-sensitive, geographically distributed, and scales linearly with users × tokens rather than stepwise with model releases. It doesn't end when the model ships.

But what if AI demand doesn't materialise at the scale being underwritten? Lend for eight years to fund a data centre that's obsolete in three, and you've made a bad trade. BlackRock and others have flagged exactly this concern, and it deserves a hearing. People look to the 1990s fibre build-out and the glut of overcapacity that resulted as a warning.

But, the evidence today cuts the other way: demand is skyrocketing and capacity is the binding constraint. The capex is racing to catch up. Anthropic planned for a 10x increase in ARR over the course of Q1 2026. It actually grew 80x (!!!!).

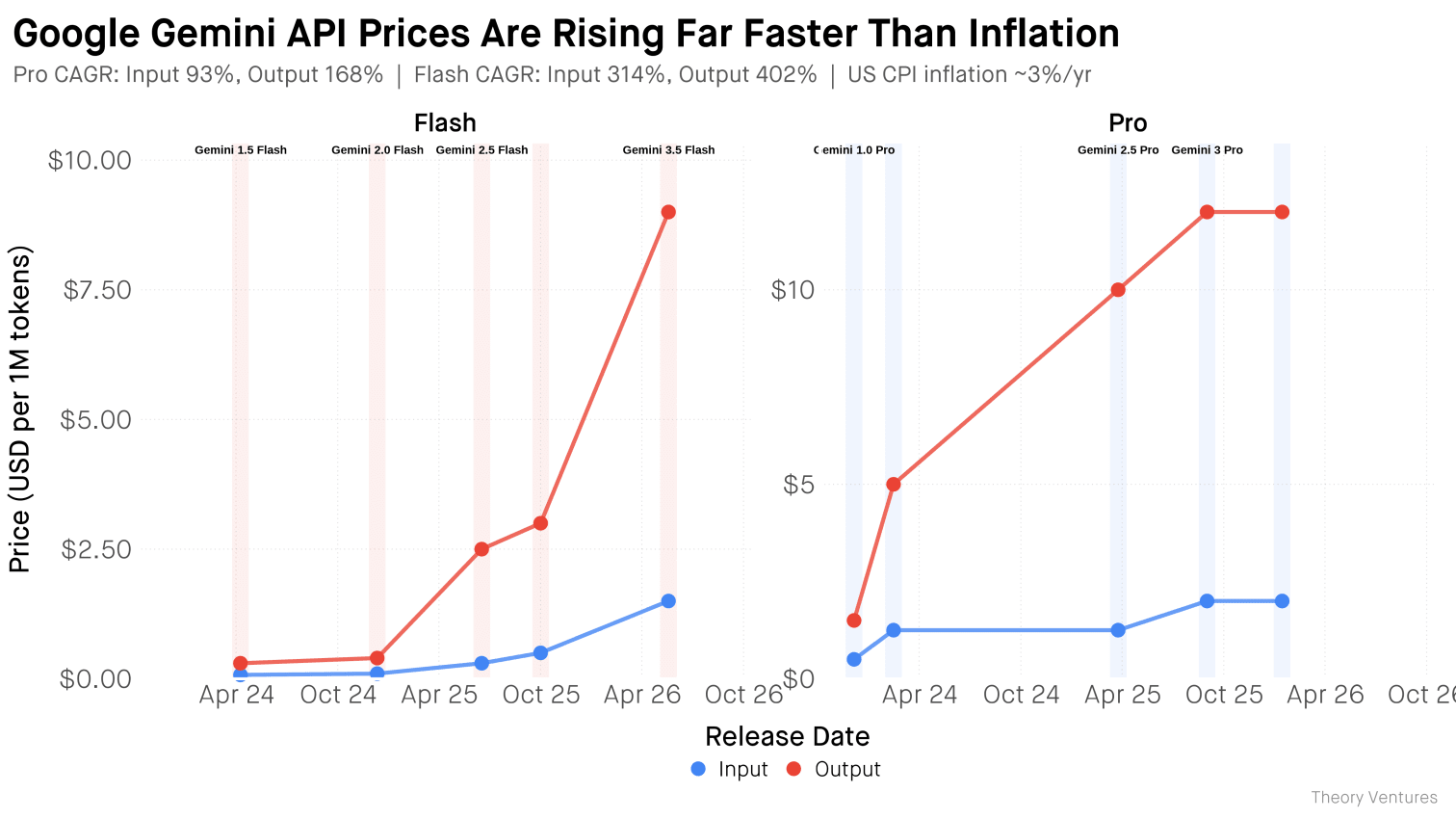

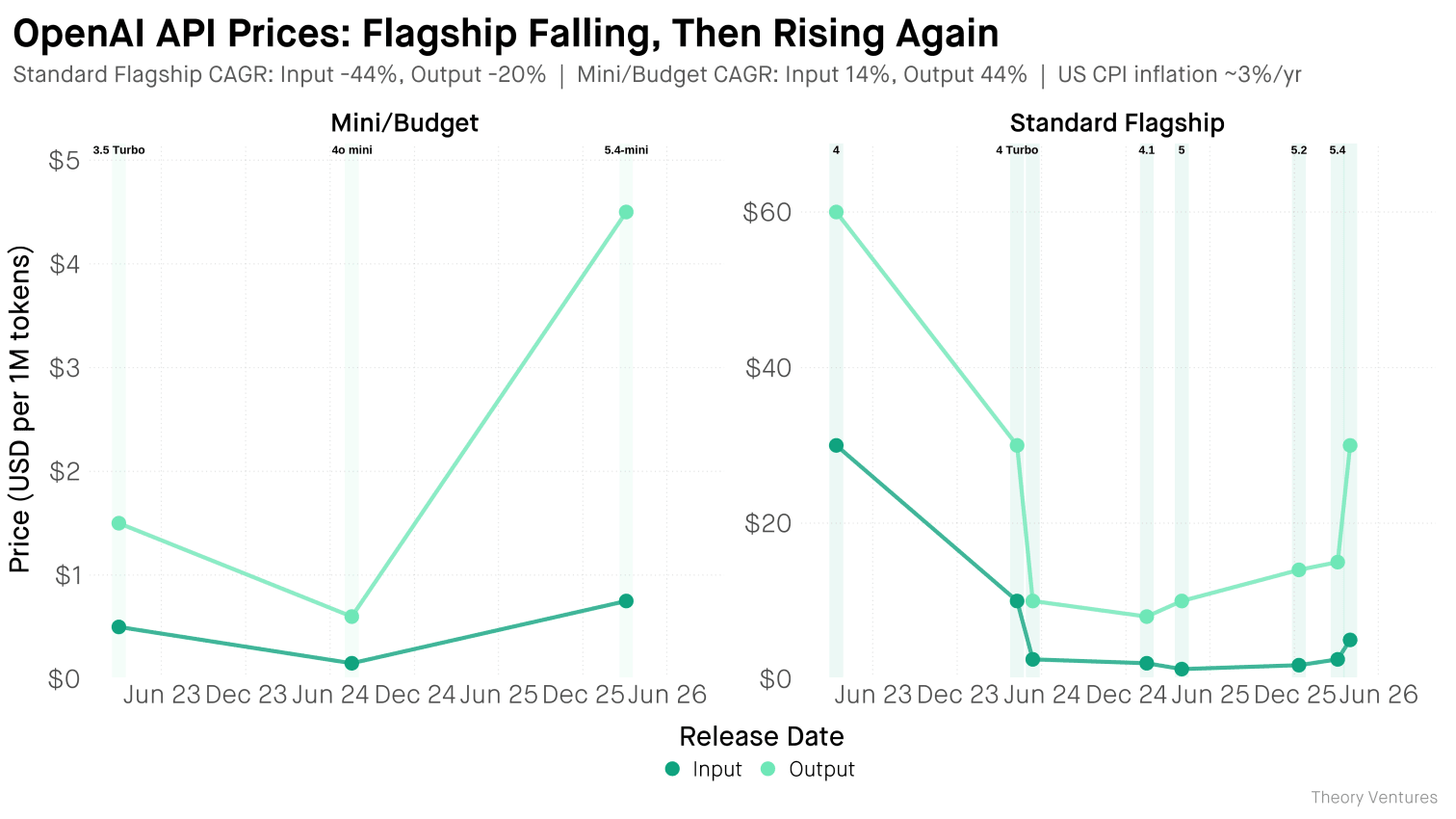

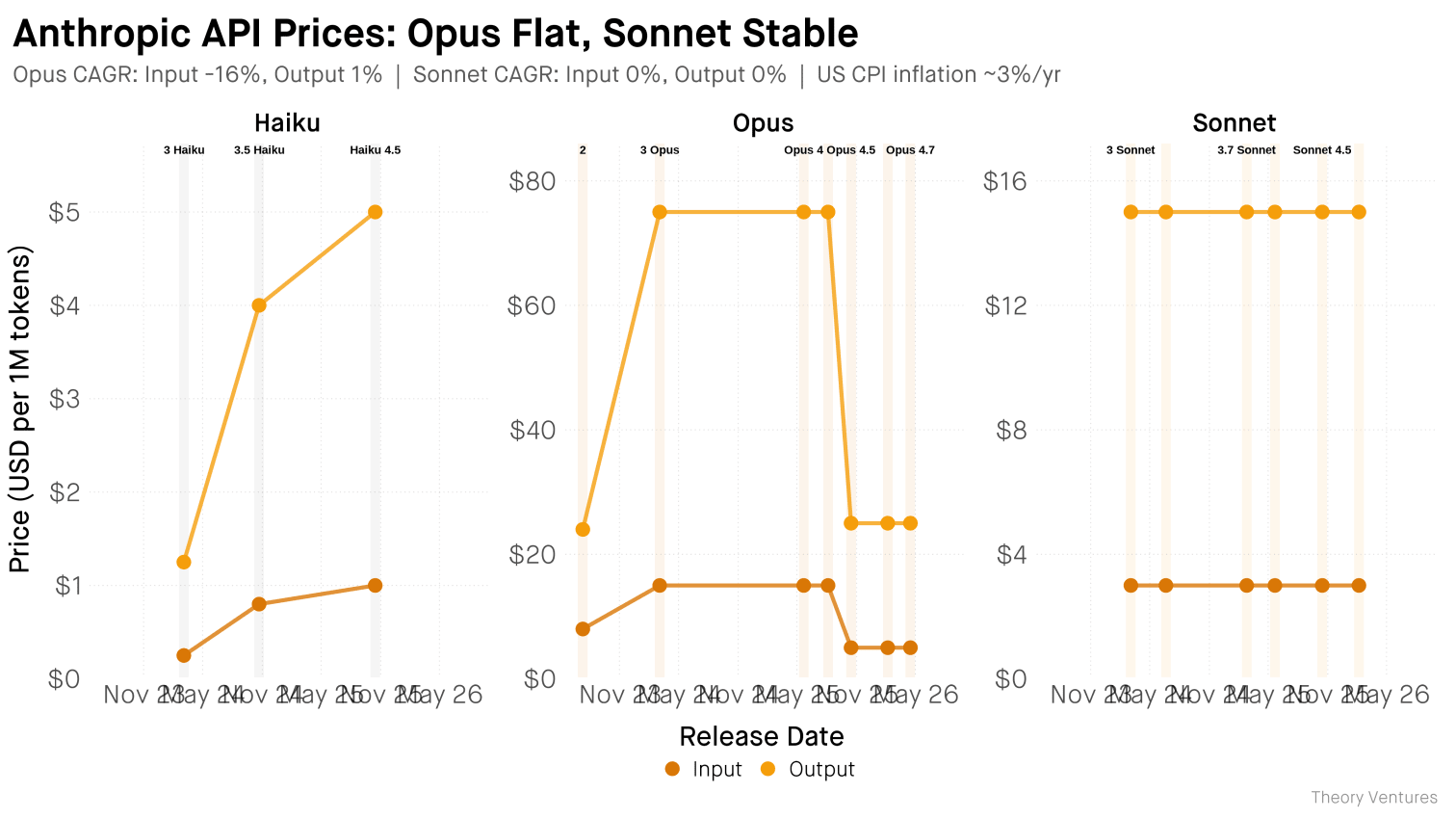

You can see it in prices. As Tomasz Tunguz from Theory Ventures pointed out this week, every frontier provider has re-rated API pricing up over the last year. Gemini's has nearly tripled.

Gemini API pricing over time. Source: Tomasz Tunguz, AI Model Inflation

OpenAI flagship model pricing over time. Source: Tomasz Tunguz, AI Model Inflation

Anthropic / Claude API pricing over time. Source: Tomasz Tunguz, AI Model Inflation

The labs spent two years subsidising usage to grab market share; at current demand loads, that's untenable. Anthropic and OpenAI are also visibly throttling: weekly rate limits on Claude Code, peak-hour slowdowns concentrated between 5am and 11am Pacific, exactly when North American and European business hours overlap and inference demand is tightest. All three flagship models are moving in the same direction at the same time, while capex spending is setting records.

The deeper point is this: the frontier models are now already so capable, that you could imagine the industry pausing training entirely and still being short of capacity. And as model capability converges, the differentiator becomes access to compute. Models, like new drugs, are extraordinarily expensive to discover and reasonably cheap to copy. What doesn't get commoditised is the GPU you need to serve a billion tokens an hour at low latency. The durable moat is increasingly steel, silicon and electricity.

A clutch of recent deals hints that the labs themselves know it. SpaceX/xAI has a decent model (Grok), but more impressively has access to huge capacity of compute through its Colossus Data Centres. (If Elon can do one thing well, it's build big expensive things in the physical world faster than anyone else thought possible). Recent deals with Anthropic and Cursor show where the moat is.

SpaceX is still loss making, but the rest of the hyperscalers are sitting on businesses that print free cash flow. Alphabet generated $165bn of operating cash flow in 2025 from search and YouTube ads; Amazon produced around $100bn of free cash flow in fiscal 2025 from retail and AWS. Those are the perfect assets to leverage against to fund this buildout.

In fact, if AI success comes down to token cost, and token cost comes down to data centre build cost (+ energy), then access to cheap capital is going to be the defining factor of long term success. Highly rated tech companies issuing long dated debt - that is some of the cheapest capital out there, certainly from private sector borrowers. In fact, Microsoft's cost of capital is close to that of the largest AAA development banks.

| Issuer | S&P | 10y yield | 20y yield |

|---|---|---|---|

| Supranationals | |||

| KfW | AAA | 4.727% | 5.023% |

| World Bank (IBRD) | AAA | 4.782% | 5.056% |

| European Investment Bank | AAA | 4.789% | 5.137% |

| Big Tech | |||

| Microsoft | AAA | 4.968% | 5.392% |

| Alphabet | AA+ | 5.071% | 5.498% |

| Amazon | AA- | 5.148% | 5.571% |

| Meta | AA- | 5.419% | 5.989% |

| Banks | |||

| JPMorgan Chase | A | 5.514% | 5.860% |

Source: Origin Platform, current interpolated yields on USD senior unsecured benchmarks closest to 10- and 20-year tenor.

Going global

Big tech is an American story, and the US Dollar bond market is the deepest IG market in the world, but it has limits. It cannot comfortably absorb $300bn a year of issuance from five companies on top of everything else it has to digest. So hyperscalers have started doing what other large sophisticated borrowers have always done: funding themselves across every major currency pool.

Alphabet, in particular, has run a remarkable tour over the last fifteen months: USD, EUR, GBP, CHF, CAD, and JPY, for roughly $50bn in proceeds. Along the way it has set the record for the largest-ever corporate sterling deal (£5.5bn), the largest-ever corporate Swiss franc deal (CHF 3bn), and a rare 100-year sterling tranche - tech's first century bond since Motorola in 1997. Amazon has debuted in euros and Swiss francs. Meta is expected to follow.

The yen deal is particularly instructive. Japanese life insurers and pension funds carry enormous long-duration JPY liabilities, and since the Bank of Japan ended its negative-rate policy, they have been short of high-quality long-dated assets to match against them. AA-rated hyperscalers issuing at 20+ year tenors are essentially the perfect counterparty.

The downstream consequences are starting to show - European, Swiss, Canadian, and Japanese institutional investors are getting structural AI exposure through fixed income for the first time.

The bond markets of the future?

For the longest time, the largest private-sector debt issuers have been financial: banks, financing arms of large conglomerates (eg GE Capital), and public sector development banks or GSEs (Fannie, Freddie, the World Bank, etc etc).

But this wasn't always the case. If you go back to the Industrial Revolution, railroads dominated the bond market in a way that's hard to imagine today. Outstanding US railroad bonds rose from roughly $1.5bn in 1871 to over $10bn by 1914 ($40bn to $320bn in today's money). To put that in context: the total US federal debt in 1914 was just $2.9bn (about $90bn today).

Today, SpaceX is raising equity because it has no choice. It's early in its commercialisation journey, and it doesn't have the free cash flow needed to underwrite serious debt yet.

But if the company delivers even half of what its prospectus describes - Starlink at global scale, orbital data centres, a lunar mass driver, (going after a total addressable market of USD 28.5 Trillion...with a T!) - its capex needs will make Alphabet's look modest. At that point, SpaceX won't just be tapping the bond market. It could end up among the largest non-sovereign issuers in the world.

The issuers reshaping the bond market today share a common profile: high-grade, frequent, multi-currency, programmatic. Connecting those types of issuers to a wide and diverse set of dealers (and through them, investors across every major capital pool) is exactly what we built Origin for. Don't be surprised if one of these names ends up on the platform sooner than you'd think.